Analysts have a consensus EPS estimate of $1.61 for the third quarter, which was $0.01 higher than their predictions of $1.60 90 days ago. Disney will report its third quarter results after the market closes.

Wolf's Den

Viewing entries in

Earnings

Analysts have a consensus EPS estimate of $1.61 for the third quarter, which was $0.01 higher than their predictions of $1.60 90 days ago. Disney will report its third quarter results after the market closes.

The consensus estimates calling for a net loss of $0.07 per share on $169.82 million in revenue for the quarter. Yelp posted a net loss of $0.02 per share on revenue of $133.91 million in the same period of last year.

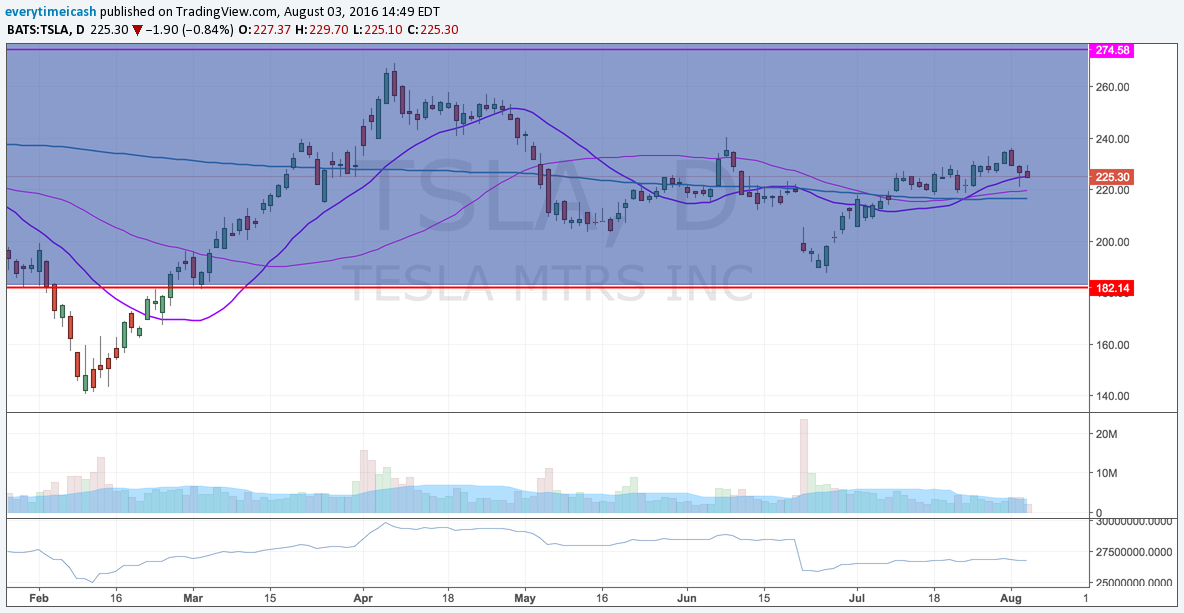

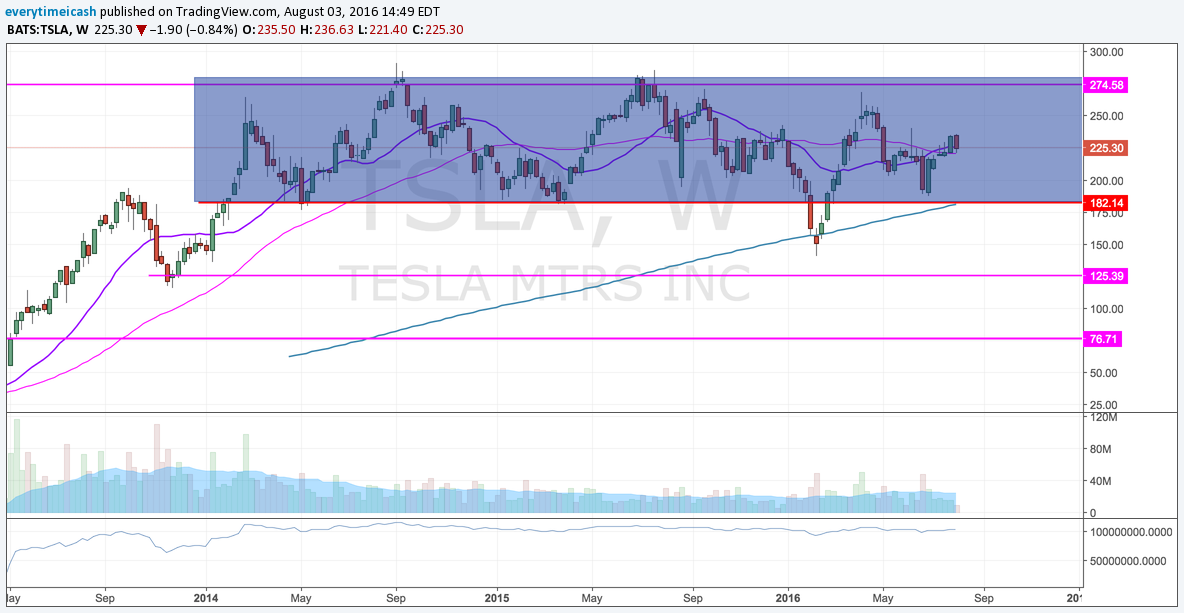

Tesla is expected to report Q2 non-GAP EPS of ($0.65) vs. ($0.48) last year with non-GAAP rev up 38% to $1.65 bln.

The stock has been very resilient despite added risks as investors give Elon Musk the benefit of the doubt.

Current Capital IQ consensus stands at EPS of $0.55 on Revenues of $862 mln.

The FSLR revenue recognition model makes it extremely difficult for analysts to provide accurate quarterly estimates. The company has been able to handily beat EPS expectations by an average of $1.03. Revenue has been a little less friendly with two big misses and three big beats over the past five quarters.

The annual projections remain the primary focus for the underlying health of the company and that is where we will be looking to judge the overall performance and outlook. Shares of FSLR have had a difficult 2016. The stock got out of the gates strong hitting a two year high of $74.29 on March 18. But the shares have tumbled 33% since that high water mark.

Shares of CAR have had a solid run since reporting Q1 results in early May. The co missed its EPS by 22 cents but revenues were in line and, most importantly, it guided FY16 revenue above the consensus. The primary driver, and what attracted investors, was commentary from the company that it was starting to see a turn around in the pricing environment for the troubled car rental business.

This stock fell from the $50 area in October of 2015 all the way to $22. So the recent upward trend allowed the stock to recapture approx 55% of its losses. But we are seeing the stock under pressure today as it has given up nearly 5% ahead of today's report. Shares are down approx 12% over the past week. This suggests that investors remain cautious on the name and are taking profits after buying low.

CAR will need to show a continued improvement in pricing to entice more investors into the name. It does have some solid support below at the 200-sma ($31.90) and the $33-34 area which both linger just below. Also we would keep an eye on Hertz (HTZ) which will trade closely with CAR on the news.

Key Metrics

Guidance

Q1 Recap

Current Quarter Expectations: As usual, operating income and revenues estimates are near the upper end of AMZN's prior guidance.

Current Capital IQ consensus stands at EPS of $8.04 on Revenue of $20.77 bln.

Key Things to Watch

Capital IQ consensus calls for Q3 adj. EPS of $0.37 on revs +3% to $3.72 bln.

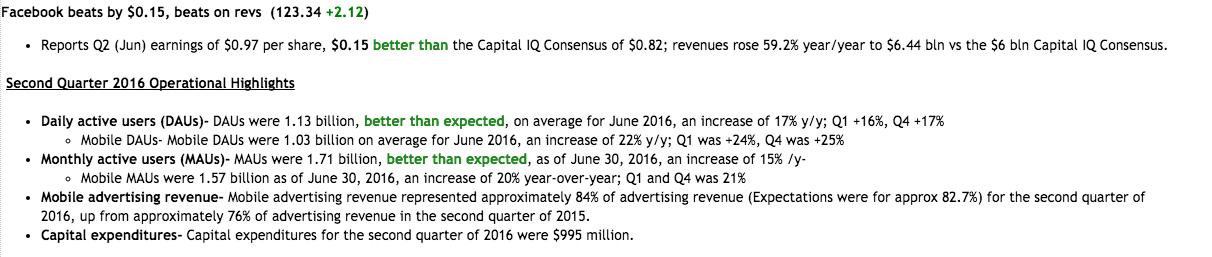

Capital IQ Consensus calls for 2Q16 EPS of $1.39 & revenue growth of 18.9%, compared to 2Q15 EPS of $1.23 on revenue of $2.28 bln.

Current Capital IQ consensus stands at EPS of $0.82 on Revenue of $6.00 bln.

Q1 Recap

Analysts are looking for Q2 adj. EPS of $0.16 with adj. EBITDA +37% to $88.8 mln and sales +16.5% Y/Y to $296.8 mln.

Match guided for Q2 dating rev +4-5% Q/Q to ~$270.8-273.4 mln with a dating EBITDA margin in the low to mid-30% range vs. 26% in Q1.

Twitter (TWTR) is set to report Q2 earnings tonight after the close with a conference call to follow at 5pm ET. Current Capital IQ consensus stands at EPS of $0.09 on Revenues of $607.4 mln.

Q3 Capital IQ consensus calls for EPS of $1.39 (versus $1.85 last year) on revenue of $42.126 bln (-27% YoY). The current consensus is near the mid-point of the company's guidance of $41-43 bln.

The current Capital IQ Consensus Estimates call for Q2 EPS of $0.94 and revenues of $3.09 bln. VZ expects full year 2016 adjusted earnings to be comparable to the co's full year 2015 adjusted earnings of $3.99 EPS

Freeport-McMoRan (FCX) is expected to report Q2 results tomorrow before the market opens with a conference call to follow at 10am ET.

FY16 Guidance

The co reiterated FY16 guidance below Consensus on April 28 when they reported 1Q16 earnings. Capital IQ Consensus calls for a 2.5% decrease in FY16 rev to ~$31.8 bln, compared to $32.6 bln in FY15.

1Q16 Recap

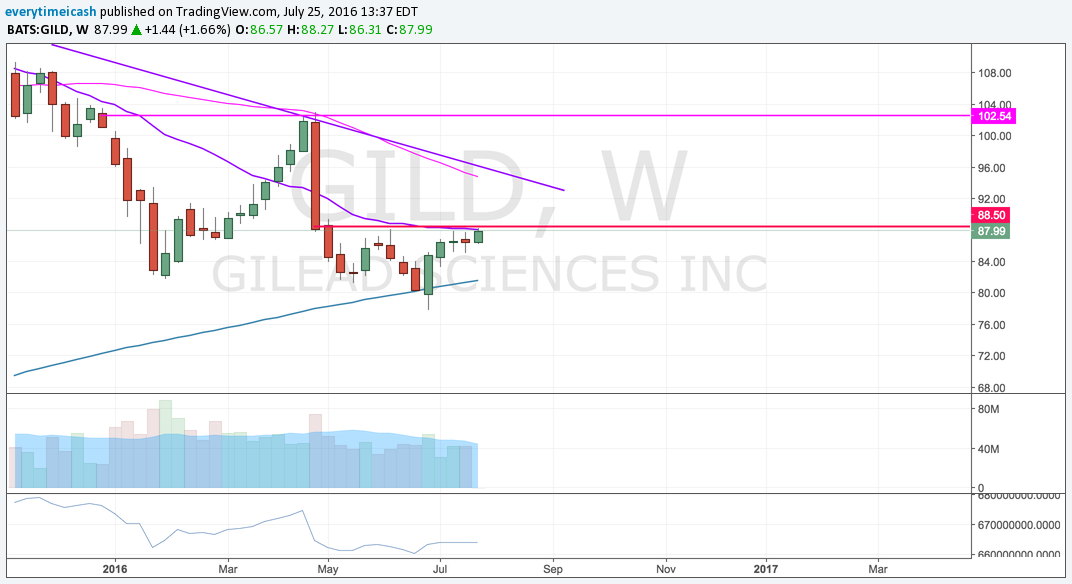

Technical Analysis

Technically, GILD has been an under-performer since its last earnings report in April had its selling back down to its early Jan/Feb lows around the $82 area. Buyers will want to clear this 87/88 resistance and lift price back into the late-April bearish gap between the 92/96 zone.

Based on GILD options, the current implied volatility stands at ~ 29%, which is 14% higher than historical volatility (over the past 30 days). Based on the GILD Weekly Jul29 $86.5 straddle, the options market is currently pricing in a move of ~5% in either direction by weekly expiration (Friday).

Last quarter, Under Armour beat Q1 EPS estimate by $0.02, reported revs in-line, guided Q2 operating income / revenues in-line and slightly raised FY16 guidance / reaffirmed margin guidance.

Headed into the print: UA has held onto these recent gains and is back near pre-Q1 levels.

Based on UA options, the current implied volatility is 14% higher than the historical volatility (over the past 30 days). UA Weekly Jul29 $42.5 straddle is currently pricing in a move of ~8% in either direction by weekly expiration (Friday).

Key metrics and areas of interest:

Techs:

Close to 40% of the S&P 500 will report their quarterly results this week. That includes McDonald's, which will report before the open on Tuesday.

Current Consensus is calling for adj EPS of $1.40 on revenues +6% Y/Y to $13.2 bln.

Q1 Expectations: EPS of $0.37 vs $0.56 year ago on sales -4.3% y/y to $5.96 bln.