WDC is expected to report second quarter earnings tonight after the close. There is a conference call scheduled for 17:00 (the company typically guides on the conference call).

Wolf's Den

Viewing entries in

Stock Market

WDC is expected to report second quarter earnings tonight after the close. There is a conference call scheduled for 17:00 (the company typically guides on the conference call).

AT&T (T) is set to report Q4 results after the bell today (4:30pm ET). Cap IQ Consensus estimates Q4 EPS of $0.66 (vs. $0.55 in 4Q15), w/revs of $42.18 bln ( ~flat y/y).

Celgene (CELG) will report Q4 results tomorrow before the market opens with a conference call to follow at 9am ET. CELG is expected to report Q4 results at 7:30am. Current Capital IQ consensus stands at EPS of $1.60 on Revenue of $3.02 bln

IBM (IBM) will report Q4 results tonight after the bell with a conference call scheduled to start at 5:00 p.m. ET. Usually, IBM reports within the first 10 minutes after the bell.

Gigamon dives -18% on guidance; trading down near $38 after-hours. Next major area of support near June's breakout. This could be a foreshadow for darling stock NVDA IF they ever miss/soften their guidance.

The market will be paying close attention to several reports from the banking industry on Friday morning. The two "most important" being Bank of America and JP Morgan.

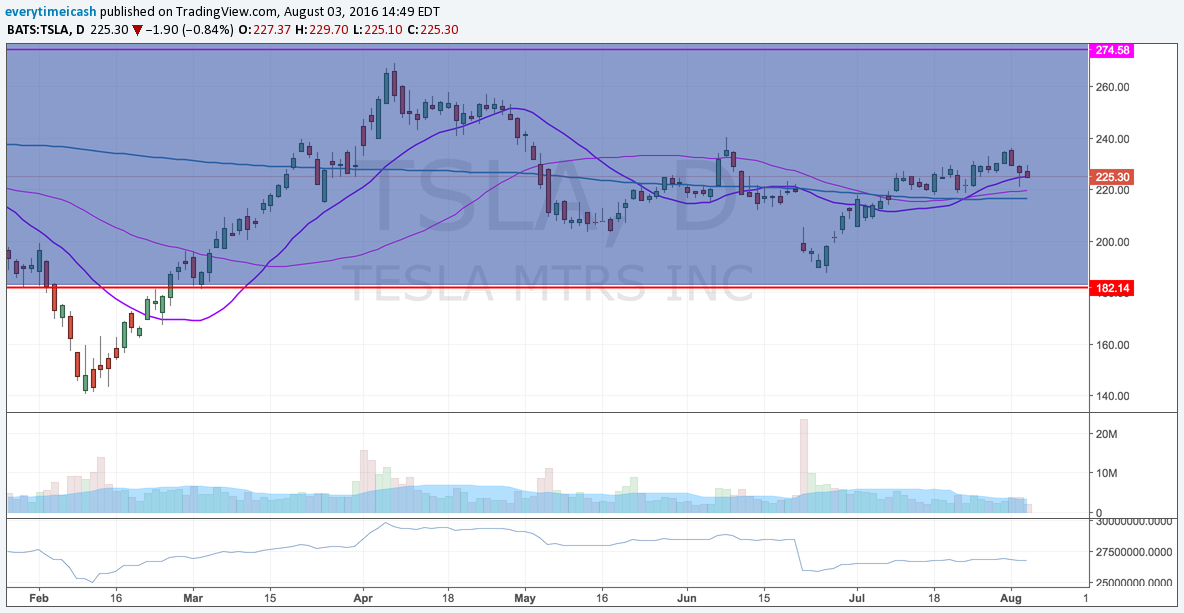

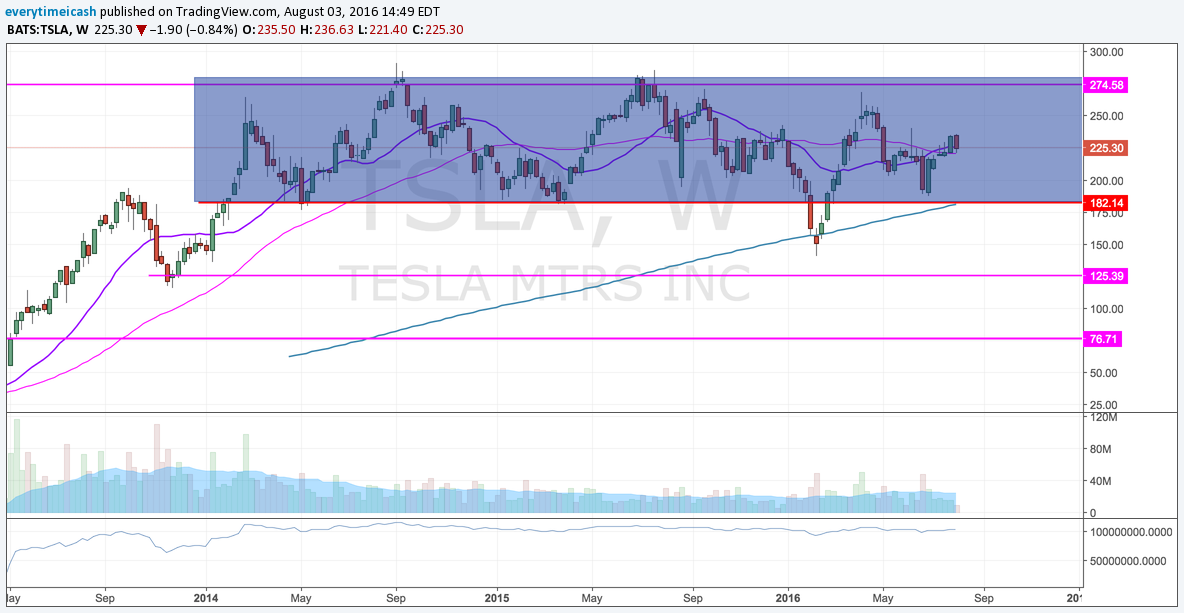

To me there are fewer setups that look as appetizing as Tesla this year. The stock has been lashed out at by bears for two years and has seemingly had everything thrown at it. With that, and barring a completely overall bear meltdown, I find it hard for the investors in the stock to ring the register this year.

TSLA has been consolidating on a monthly basis.

With the slated Model 3 deliveries, 2017 marks the year that the Tesla mass consumer comes online. With that comes a new revenue stream and the growth dynamic back into play.

The automaker took 400,000 pre-orders for the Model 3 within weeks of revealing the prototype. The main issue they face is producing millions of them, on time, up to quality standards, and most importantly; without losing money. Tesla doubled their production in 2016 to 100,000 cars. In April, Musk said he wants to produce half a million cars by 2020. One month later, he said they’d get there by 2018. Aggressive as that may be, Musk seems to deliver under pressure. The Model 3’s biggest hinderance on performance deliveries are projections, expectations, and supply chain. With expectations coming as a result of projections, supply chain will be your tell with the company’s ability to deliver results.

Many analysts who bash Tesla’s stock will have you know that there is a steady increase in competition in recent years. They’re full of shit. Tesla operates in the high end electric vehicle market. Until now, they’ve been the only real player. Recently Fisker, Farady Future , and Lucid Motors have perked up to compete but until now there really hasn’t been a viable competitor.

The main difference however is that Tesla has centered itself on building a network and working outward. SImilar to the Apple vs everybody model, Tesla has open sourced its technology and focused its attention on building a sustainable network/brand first then focus on its product offerings. That’s why the term “Cult Stock” has often been used to describe the company/stock.

As I’ve said above, Tesla has been range bound for nearly two years now. In early 2015, the stock broke it’s 180 “support” level and found itself bouncing sharply off of its 200 week MA. Since then the stock made a high at nearly 270 and then a failure and hold of the 180 level yet again. As of late the stock has once again broken out of its downtrend and appears to be acting constructively. With the addition of Elon Musk to the Trump Advisory team, the short interest, new product offering, and constructive behavior, this stock is set to rip in 2017.

One key amendment to this argument is the price of oil. Which since the Barron’s $20 oil cover, has been constructive and working its way higher. All of these instances bode well for Tesla which I believe has a very defined stop ($180) and a potential to break out to an all time high.

TSLA’s gigafactory goes active in 2017 making them the largest battery operator/manufacturer in the world. This will provide countless jobs as well as margin expansion. This will likely bode well for TSLA moving forward with the Trump Administration and as such bears are going to get squeezed.

To play this stock’s potential, I’ll be putting on a leaped call spread (bullish risk reversal) with the Jan 2019 350 C being bought and the Jan 19 100 P being sold. (You can also buy a lower put strike to hedge your downside risk as well.) This prices that Tesla will see a 50% gain in the next two years which “sounds crazy” but isn’t anywhere near crazy given this stock’s price action/ability. At the time of writing, this position cost a net debit of ~$2.2.

Guidance

Q2

FY17

Options Activity

TECHS:

Last week's downgrade took the wind out of the stock. Sellers responded with an aggressive drop below its rising 50-day moving average which has price in "no-man's land" ahead of earnings. Next key support is the 200-day simple ma near 73.

Shares of GOOGL hit an all time high of $838.50 on Monday but we have seen some profit taking ahead of tonight's report as the stock has pulled back to $820. The company is coming of an impressive Q2 in which it was able to accelerate revenue growth to over 20% for the first time in three years.

The growth was driven by Google website revenues as strength in the mobile and YouTube segments provided a boost. The rise in mobile has also boosted the growth in partners and website TAC which will be an area to watch.

The all time high will certainly be in play, especially when one views the Forward P/E of 20.5x being reasonable for a co that is posting 20%+ revenue increases despite being a $20+ bln a quarter company, no easy feat. A miss by GOOGL should prove interesting with the $783.50 Post-Q2 results being a key level of support. A break of this will send the shares to the $760 with the 200-sm ($757.29) in play.

Key Metrics

Q2 Recap

GOOGL reported Q2 (Jun) earnings of $8.42 per share, $0.38 better than the Capital IQ Consensus of $8.04. Revenues rose 21.3% year/year to $21.5 bln vs the $20.77 bln Capital IQ Consensus.

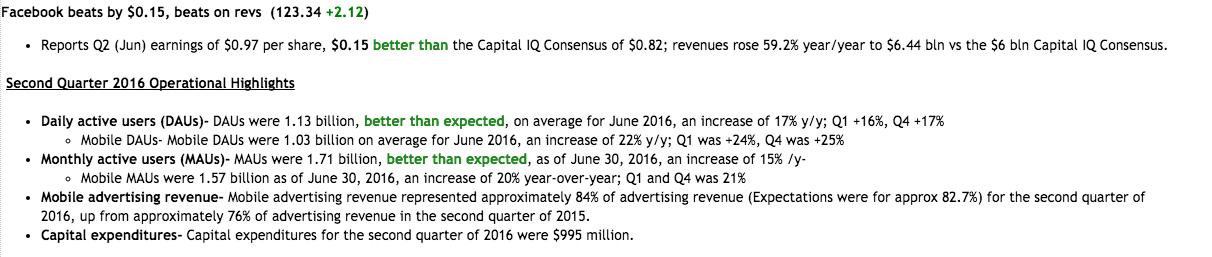

GOOGL/GOOG beats by $0.46, beats on revs

Analysts have a consensus EPS estimate of $1.61 for the third quarter, which was $0.01 higher than their predictions of $1.60 90 days ago. Disney will report its third quarter results after the market closes.

The consensus estimates calling for a net loss of $0.07 per share on $169.82 million in revenue for the quarter. Yelp posted a net loss of $0.02 per share on revenue of $133.91 million in the same period of last year.

Tesla is expected to report Q2 non-GAP EPS of ($0.65) vs. ($0.48) last year with non-GAAP rev up 38% to $1.65 bln.

The stock has been very resilient despite added risks as investors give Elon Musk the benefit of the doubt.

Current Capital IQ consensus stands at EPS of $0.55 on Revenues of $862 mln.

The FSLR revenue recognition model makes it extremely difficult for analysts to provide accurate quarterly estimates. The company has been able to handily beat EPS expectations by an average of $1.03. Revenue has been a little less friendly with two big misses and three big beats over the past five quarters.

The annual projections remain the primary focus for the underlying health of the company and that is where we will be looking to judge the overall performance and outlook. Shares of FSLR have had a difficult 2016. The stock got out of the gates strong hitting a two year high of $74.29 on March 18. But the shares have tumbled 33% since that high water mark.

Current Quarter Expectations: As usual, operating income and revenues estimates are near the upper end of AMZN's prior guidance.

Current Capital IQ consensus stands at EPS of $8.04 on Revenue of $20.77 bln.

Key Things to Watch

Current Capital IQ consensus stands at EPS of $0.82 on Revenue of $6.00 bln.

Q1 Recap

Q3 Capital IQ consensus calls for EPS of $1.39 (versus $1.85 last year) on revenue of $42.126 bln (-27% YoY). The current consensus is near the mid-point of the company's guidance of $41-43 bln.

The current Capital IQ Consensus Estimates call for Q2 EPS of $0.94 and revenues of $3.09 bln. VZ expects full year 2016 adjusted earnings to be comparable to the co's full year 2015 adjusted earnings of $3.99 EPS

Last quarter, Under Armour beat Q1 EPS estimate by $0.02, reported revs in-line, guided Q2 operating income / revenues in-line and slightly raised FY16 guidance / reaffirmed margin guidance.

Headed into the print: UA has held onto these recent gains and is back near pre-Q1 levels.

Based on UA options, the current implied volatility is 14% higher than the historical volatility (over the past 30 days). UA Weekly Jul29 $42.5 straddle is currently pricing in a move of ~8% in either direction by weekly expiration (Friday).

Key metrics and areas of interest:

Techs:

Close to 40% of the S&P 500 will report their quarterly results this week. That includes McDonald's, which will report before the open on Tuesday.