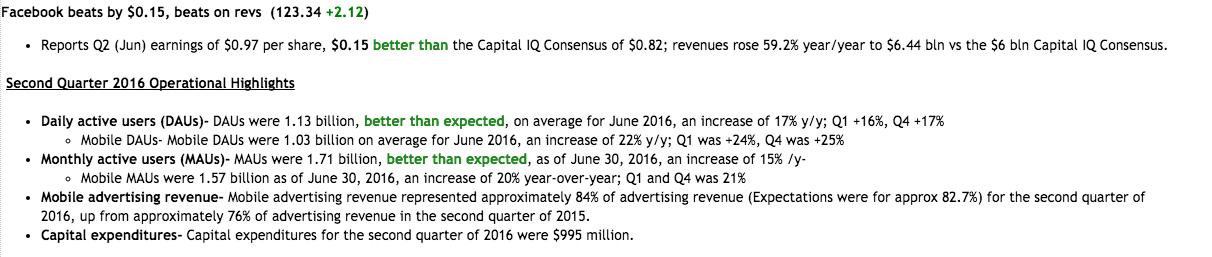

Facebook (FB) is set to report Q2 results tonight after the close with a conference call to follow at 5pm ET.

Current Capital IQ consensus stands at EPS of $0.82 on Revenue of $6.00 bln.

- Revenue Growth- Q1 revenue growth was 51.8%; Q4 saw revenue accelerate to 52% compared to 40% in Q3 and 39% in Q2.

- Advertising Revenue- Q1 increased 57% y/y to $5.2 bln; Q4 came in at $5.637 bln which was also up 57% y/y.

- Mobile Advertising Revenue- Mobile advertising revenue represented approximately 82% of revenue in Q1 compared to 80% in Q4. This is expected to see a small uptick.

Q1 Recap

- FB reported Q1 (Mar) earnings of $0.77 per share, $0.15 better than the Capital IQ Consensus of $0.62; revenues rose 51.8% year/year to $5.38 bln vs the $5.26 bln Capital IQ Consensus.

- See key metrics above.

- FB also announced its proposal of a new class of stock so look for some updates on this on the call.

- Why it's important

- Ad spending drives Facebook's top line, accounting for 97% of the company's revenue in the first quarter. Facebook, therefore, is watched closely as a barometer for how advertisers are spending and where they are allocating their advertising budgets.

- Facebook is a leadership stock for the Nasdaq and Nasdaq 100

- The company and its stock serve as guides for the enthusiasm surrounding the growth of social media

- What Facebook said after its first quarter earnings report in April

- Daily active users (DAUs) were 1.09 billion on average for March 2016 (+16% year-over-year); mobile DAUs were 989 million on average for March 2016 (+24% year-over-year)

- Monthly active users (MAUs) were 1.65 billion as of March 31, 2016 (+15% year-over-year); mobile MAUs were 1.51 billion (+21% year-over-year)

- The average price per ad increased 5% in the first quarter while total ad impressions increased 50% (strong growth in mobile ad impressions)

- Will face tougher comparisons in 2016 given the acceleration of ad growth in 2015

- Guidance

- Non-GAAP expense growth of ~45-55% year-over-year

- Amortization will be $700 million to $800 million

- Stock-based compensation to be $1.1 billion to $1.3 billion in 2016

- Sees capex at the high end of $4.0 billion to $4.5 billion range previously provided

- Second quarter and FY16 tax rates should be similar to first quarter

- Other Stocks to Watch

- FB

- Alphabet (GOOG/GOOGL)

- LinkedIn (LNKD)

- Yelp (YELP)

- PowerShares QQQ Trust (QQQ)

- Global X Social Media Index ETF (SOCL)

- FB is third largest holding at 9.37% of assets

- S&P futures

Click here to listen to my podcast and learn about my theory on the similarities between relationships and the stock market.

RESULTS: