Coca-Cola (KO) is scheduled to report Q1 earnings tomorrow, before the opening bell, at 6:55 ET.

Current Consensus is for Q1 EPS of $0.44 (-8% Y/Y) on revenues of $10.2 bln (-5% Y/Y).

Current Consensus is for FY 16 EPS $1.95 on revs of $42.3 bln

Last quarter, KO beat EPS by $0.01/share w/ revs in-line.

FY 16 Guidance from Last Q

- Organic revs expected to grow 4-5%

- Expects currency neutral income before tax, structurally-adjusted to grow 6-8% in 2016

- Expects net impact of acquisitions and divestitures to be a four-five point headwind to net revs

- Expect ~$2-2.5 bln in net share repurchases in 2016

- Expect comparable currency neutral EPS growth of 4-6%

- Expect to spend $2.5-3 bln on capex

- Due to structural changes, co anticipates slightly higher COGS and SG&A

- Co expect the benefit to equity income from Monster, Coca-Cola Beverages Africa and Coca-Cola European Partners to partially offset that impact at operating income, resulting in a three to four point negative structural impact to income before tax.

- Look for updates on the below two l/t initiatives

- $3 bln in productivity savings

- Additional Notables from Last Quarter

- Unit case volume was +3% YoY for Q4, and +2% YoY for FY 15

- Global price/mix grew 2% for quarter and FY 15

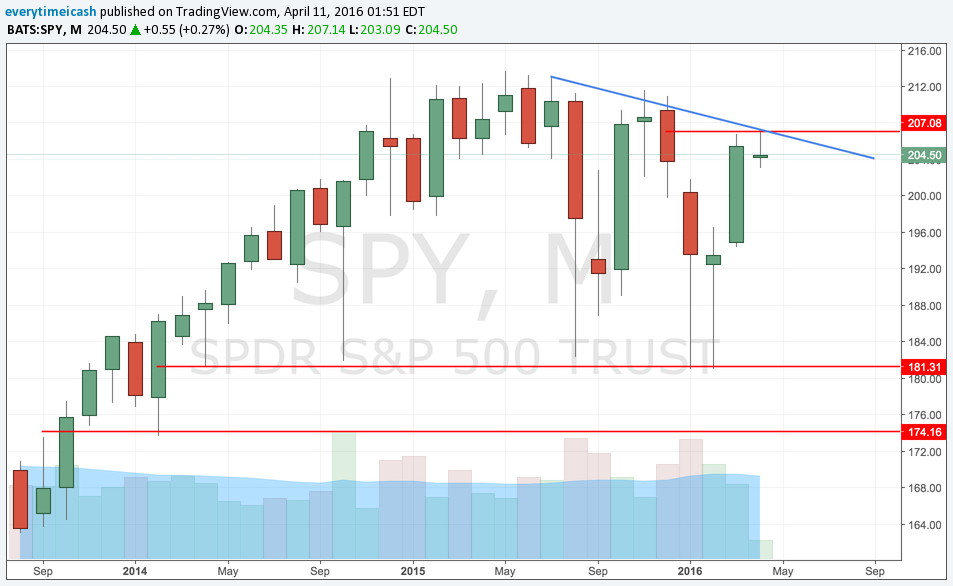

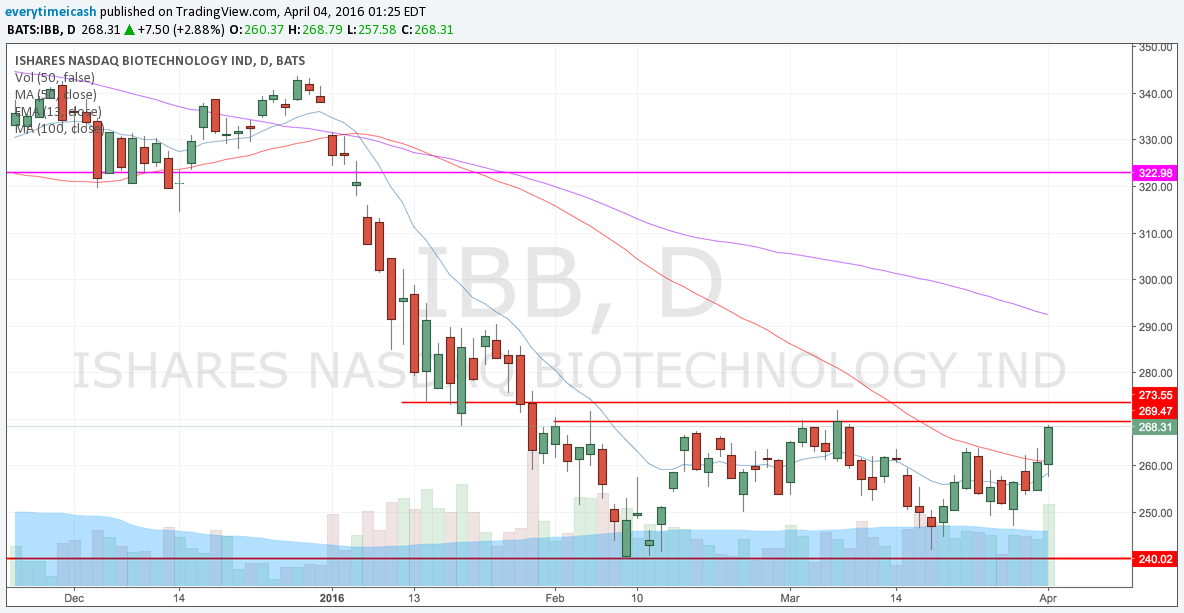

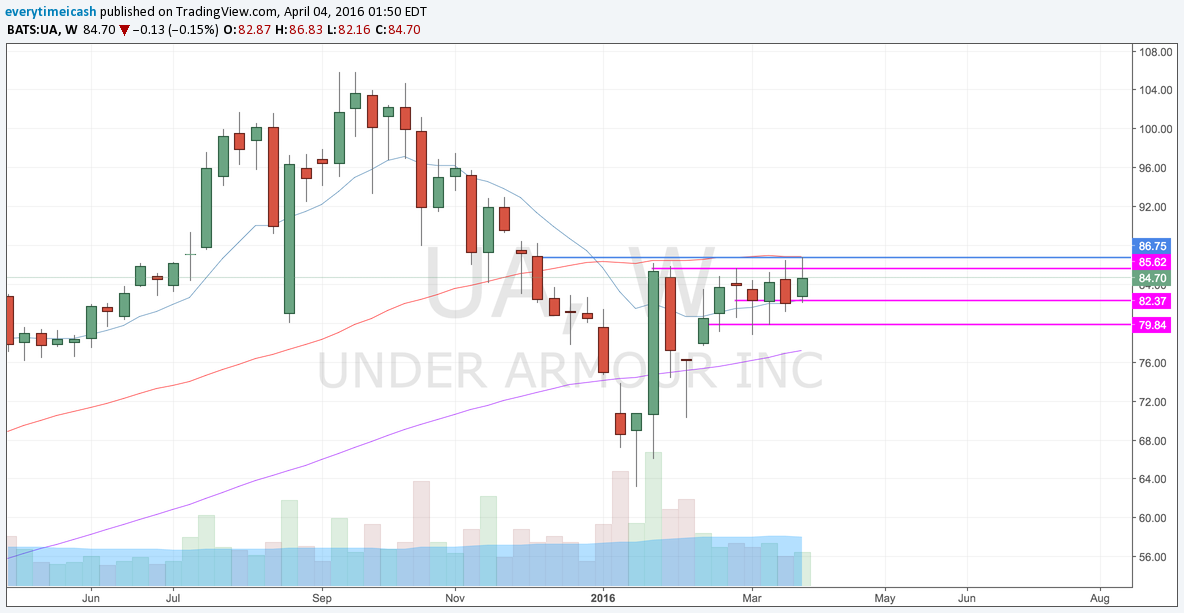

TECHS

The stock price has been in a steady uptrend since, rallying bounce on the 50 day 3 times during the last quarter. The stock is currently up ~9% on the quarter and is near its 50 day.